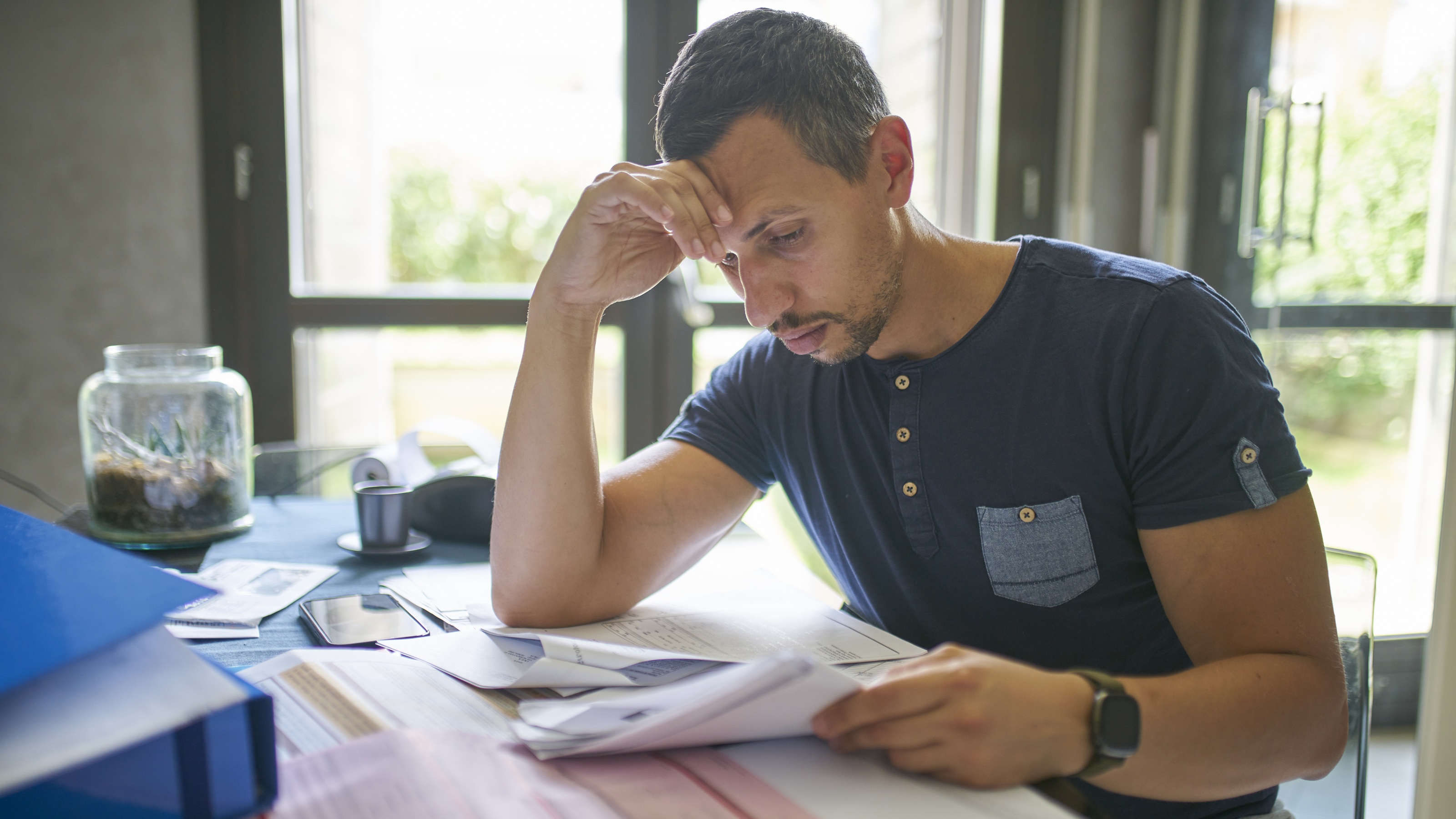

Retiring earlier than expected isn’t a new phenomenon. In fact, half of current retirees said they retired early, according to a new study by Allianz Life. Some people are pleasantly surprised to find they are financially ready even earlier than expected. Some have just had it with the 9-5 grind and are ready to leave the workforce. But for many others, there is a much different reality.

In fact, the majority of people in the study say they actually retired for reasons completely outside of their control, whether they were ready to or not. Like the 34% who said they lost their job unexpectedly or the 25% who said they had health care issues that prevented them from doing their job.

What makes this even more surprising is that this data was gathered before the coronavirus pandemic hit the U.S., which means that with high and growing unemployment data, the situation is likely even worse now. These specific risks to retirement security are likely to become exacerbated as millions lose their jobs. Ultimately, this may push more people toward retirement, sometimes well before their planned start date and often without any choice in the matter.

Sign up for Kiplinger’s Free E-Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more - straight to your e-mail.

Profit and prosper with the best of expert advice - straight to your e-mail.

So how can people deal with an early and unexpected retirement? First and foremost, stay calm. Second, make a plan.

Filling in the gaps

First, health care. If you retire earlier than planned, you may not yet be eligible for Medicare, which kicks in at age 65, so you will need to look into how you will pay for your health care coverage. This could mean determining if you’re eligible for a Consolidated Omnibus Budget Reconciliation Act (COBRA) plan from your former employer, being added to a spouse’s plan through their employer, or purchasing coverage through the Affordable Care Act federal exchange or your state’s health care marketplace.

Determine your additional health care needs and any supplemental plans you may need, like dental care. Also, never underestimate the potential cost of health care in retirement. You will find yourself needing more health care services as you age, and it is not going to get any cheaper.

You may also be looking at claiming Social Security earlier than planned to help make up for lost income. While you might not have a choice and need the money now, if you are still able to delay starting your payments — even by a few months — you will boost the check you get from Social Security. Talking to a financial adviser specializing in Social Security can help you map out a strategy for when and how to take payments.

Explore other employment options

If you’re finding yourself in retirement before you were really “ready,” you may decide to look for another job — perhaps part time or hourly — either to help keep yourself busy, to bring in extra income, or get employer-sponsored health insurance. If you or your spouse are under 65 then you must find health care coverage until you can apply for Medicare at age 65. In the study, nearly two-thirds (65%) of people not yet retired believe it is likely they will work at least part time in retirement, but in reality, only 7% of retirees say they are currently working at least part time.

In light of the current economic situation and increasing numbers of people filing for unemployment, more retirees may choose to look for work in retirement to make more money. While some of those gig or hourly jobs might be tough to come by right now, keep an open mind about taking on a job perhaps in the future once the economy starts to bounce back. Not only can it help make up for some of the lost income you were planning on from your last job, but it can also help keep you mentally and physically fit.

Consider retirement income

Adjusting to not getting a regular paycheck in retirement can be a challenge. For some, incorporating a financial product like an annuity that offers guaranteed retirement income could be a solution that not only helps address the financial aspect of lost income, but can also provide reassurance that comes with guaranteed income for life. Not only do annuities provide income that can help address gaps due to no longer receiving a steady paycheck, but they can also provide a level of protection against market downturns like we have seen over the past few weeks.

Yet, only 30% of not-yet-retired people say they currently have a source of guaranteed income in their portfolio to help them meet retirement goals. And while 39% say they plan to purchase a guaranteed income product in the future, only 3% view it as a top priority.

Working with a financial professional, you can determine if a guaranteed income product makes sense for your financial situation.

A long road ahead

While no one can be sure what will happen next with the economy or the current COVID-19 pandemic, there are things we can do now to help set us up to manage retirement risks in the future. While saving and planning for retirement might not seem like a priority right now amid many of the other things happening in the world, it remains important. By having a strategy in place, you can be better prepared for whatever curveball might come next.

Annuity guarantees are backed by the issuing company.

-

Stock Market Today: Solid Signals Lift Stocks Despite Tariff Noise

Stock Market Today: Solid Signals Lift Stocks Despite Tariff NoiseMarkets are whistling over the White House in an ongoing display of corporate America's enduring ability to survive and advance.

-

Amtrak Joins Prime Day With Deals on Fares — But You’ll Have to Act Fast

Amtrak Joins Prime Day With Deals on Fares — But You’ll Have to Act FastPrime members can score 20% off midweek fares — what travelers should know before booking.

-

Key to Financial Peace of Mind: Think 'What's Next?' Rather Than 'What If?'

Key to Financial Peace of Mind: Think 'What's Next?' Rather Than 'What If?'Even if you've hit your magic number for retirement, it's hard to stop worrying about money. Giving it a clear purpose is one way to reduce financial anxiety.

-

Three Estate Planning Documents a Business Owner Can't Afford to Skip

Three Estate Planning Documents a Business Owner Can't Afford to SkipA business owner's estate plan should protect the company and its employees as well as the entrepreneur's heirs. These three documents are critical.

-

Financial Fact vs Fiction: Why Your 'Magic Number' Isn't Actually Magical

Financial Fact vs Fiction: Why Your 'Magic Number' Isn't Actually MagicalDo you think you're diversified if you're invested in the S&P 500 and Nasdaq? Do you think your tax rate will fall in retirement? Think again — and read on for other myths that could be leading you astray.

-

Opportunity Zones: An Expert Guide to the Changes in the One Big Beautiful Bill

Opportunity Zones: An Expert Guide to the Changes in the One Big Beautiful BillThe law makes opportunity zones permanent, creates enhanced tax benefits for rural investments and opens up new strategies for investors to combine community development with significant tax advantages.

-

Five Ways Retirees Can Keep Perspective Through Market Jitters

Five Ways Retirees Can Keep Perspective Through Market JittersMarket volatility is a recurring event with historical precedents (the dot-com bubble, global financial crisis and pandemic), each followed by recovery. Here's how people who are near or in retirement can navigate economic uncertainty.

-

I'm a Financial Strategist: This Is the Investment Trap That Keeps Smart Investors on the Sidelines

I'm a Financial Strategist: This Is the Investment Trap That Keeps Smart Investors on the SidelinesForget FOMO. FOGI — Fear of Getting In — is the feeling you need to learn how to manage so you don't miss out on future investment gains.

-

Can You Be a Good Parent to an Only Child When You're Also a Business Owner?

Can You Be a Good Parent to an Only Child When You're Also a Business Owner?Author and social psychologist Susan Newman offers advice to business-owner parents on how to raise a well-adjusted single child by avoiding overcompensation and encouraging chores.

-

How Advisers Can Steer Their Clients Through Market Volatility (and Strengthen Their Relationships)

How Advisers Can Steer Their Clients Through Market Volatility (and Strengthen Their Relationships)Financial advisers need to be strategic when they communicate with clients during market volatility. The goal is to not only reassure them but to also help them avoid rash decisions, deepen your relationship with them and build lasting trust.